A. CO-PURCHASING

You would be hard-pressed to find a co-op that allows a parent to be the sole owner while a child occupies the apartment - or, in reverse, allows parents to appear on the application without being recorded on the deed. That said, this does not relegate you to condos exclusively.

B. GIFTING

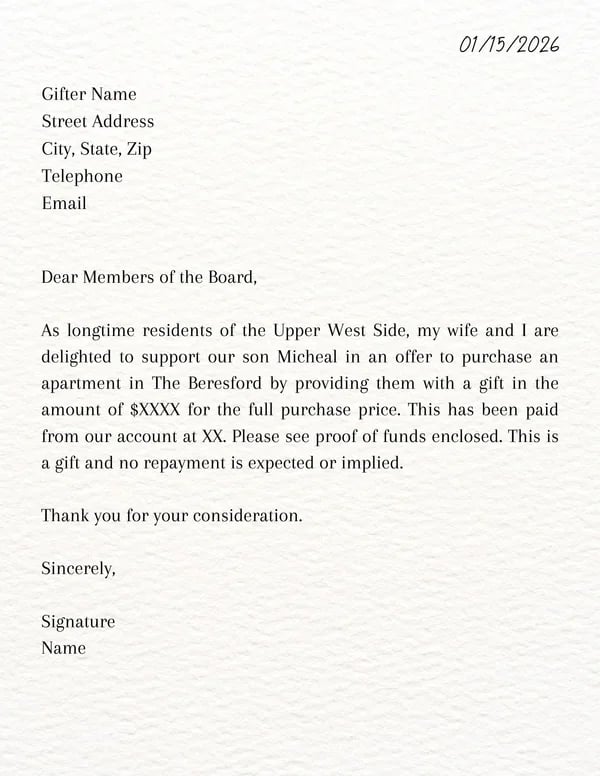

We often see parents gift a significant portion of the purchase price to their child, leaving their offspring responsible only for the monthly maintenance and little or no mortgage payment.

From the co-ops perspective, this must always be a “gift” and not a “loan” to the child. Although some families make their own behind-the-scenes arrangements, the gift-giver must always provide a letter promising that no repayment is expected, and also share “proof of the funds” that they are gifting. We will guide you through viable options for each given scenario.

C. CONDOS

One of the many reasons condos are more expensive than co-ops is the flexibility they offer in situations like this. Anyone can purchase the home with little scrutiny of their financial situation, and anyone can occupy the property.

While many buyers find this limits their choices (because they want a quintessential SoHo artist’s loft or a prewar fireplace in the Village and most of these options are co-ops) - condos remain the best choice for maximum ease and they are often the only viable option for international buyers, ultra-private individuals, or those with non-traditional income that doesn’t fit the co-op mold. Buying a condo can also allow the parents to provide a long-term investment for the child, even if they move elsewhere in the future.

BONUS BARRIERS

Certain buildings, particularly those near universities, may have bylaws that specifically prohibit parents buying for children, with the goal of preventing the building from becoming dorm-like. Some buyers try to “fudge” their profile by presenting an offer that claims the parents are purchasing a pied-à-terre, only to have the college freshman be the one actually moving in. But boards are on the lookout for this and can usually spot the subterfuge quickly. We prefer to find creative and transparent solutions for getting our clients into the home they want, with no room for error.

More restrictive co-ops, particularly on Park or Fifth Avenue or Central Park West, do not permit any of these scenarios at all. So we will steer you clear of these from the very start.

Now the deal is struck, contracts are signed, and it is time for the board application. We only let clients get to this point once we are certain that the purchase structure aligns with the building’s requirements, and then we proceed with extra care, knowing there may be additional scrutiny from the board. Regardless of how incredibly successful and established or even fully middle-aged the “child” may be, our 'watchful care' continues to create long line of happy homeowners.