YOU CAN PROBABLY CHILL (FOR AT LEAST A COUPLE OF YEARS)

The following newsletter will explain the mechanics of the new tax on properties that are not occupied as a primary residence (approved just last week, taking effect July 1), along with some additional intel that may dispel some of the industry-induced panic:

PHASE 1:

In the first phase of this tax (now until June 2028), the calculation for condos and co-ops is based on existing and antiquated Department of Finance assessments found on the property tax bill, and they are WAY less than the actual value.

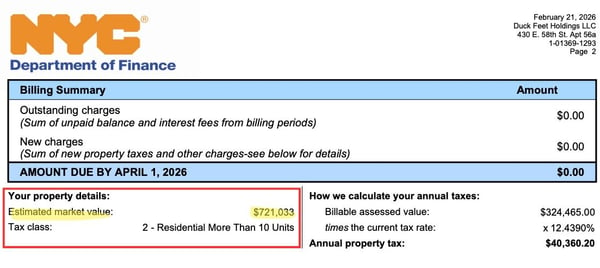

Example: Earlier this year, my California clients purchased a new development condo for $6,500,000 as their pied-à-terre. However, the current estimated market value on the tax record is $721,033, which is below the million-dollar threshold that triggers the tax.

Below is 15A at Walker Tower. It's on the market now asking $11,995,000. The assessed DOF market value is $856,172. Also exempt.

__________________________________________

This gorgeous prewar condo at 36 Bleecker just went into contract, asking $10,000,000. Its assessed market value is $1,567,092. This illustrates how chaotic the DOF values are.

So for the first phase, the rate of the new tax is very high because it’s calculated on these much lower valuations.

- 4% on values between $1M–$3M

- 5.25% from $3M–$5M

- 6.5% above $5M

This Penthouse with a wild curly slide is under contract for $20 million. Its DOF assessed value is $1,913,891. Its new tax would be 4% of that, equaling, an additional $76,555 annually, in addition to their regular property taxes, which are $230,963.

Single-family and 1–3 family homes, which have more accurate tax assessments are totally exempt below a $5M threshold. Those above that will be taxed at rates ranging from 0.80% to 1.30%.

PHASE 2

The pied-à-terre tax calculation will now be based on a comparable-sales valuation approach. How they are going to accomplish that fairly, I do not know, but they will still likely reflect more accurate market values. The tax now won’t apply to any property worth less than $5m. So it will apply to the examples listed above that were exempt in phase 1, but now the rates drop to the 0.80%–1.30% range across all property types.

Revisiting our example above at 36 Bleecker, which sold for $10m, their total taxes would double, with $80,000 added onto their current property taxes of $82,851.

The curly slide at 150 Nassau will see its pied a terre tax jump from $76k in phase 1 to $210k in phase 2.

These example calculations all assume that these properties are second homes, which few $20m apartments are, but you get the math.

PROVING PRIMARY RESIDENCE

The plan now is that DOF will issue initial notices by August 30, 2026 to owners it believes are subject to the surcharge. Owners can challenge that determination by proving primary residency — through state tax returns showing the property as their primary address, evidence that a qualifying tenant occupies the unit, or other acceptable documentation. Notably, the City has access to state income tax records to verify residency claims, and certifications can be audited for up to six years. The loopholes are, so far, non-existent, according to internal calls with our attorneys.

CO-OP COMPLEXITY

Because co-ops are assessed as single buildings rather than individual units, calculating a units DOF value and assessing the tax will be done by dividing the building's total assessed value proportionally by share allocation, requiring a dive into the corporation’s offering plan.

The pied-à-terre tax is then billed to the co-op corporation as a whole, and the board is required to collect from each affected shareholder. This creates additional risk for co-op boards because If an affected shareholder fails to pay, the corporation remains responsible for satisfying the obligation, and unpaid charges could ultimately result in a lien against the building.

Boards are advised to update proprietary leases and house rules now to address annual certification requirements and payment recovery mechanisms. Will they also stop allowing new pied-à-terre purchases?

QUESTIONS REMAIN

-

What happens if a seller is a pied-a-terre and the buyer is not or vice versa? How will the tax be pro-rated?

-

If a rental tenant uses the apartment as their pied-à-terre, will the owner be subject to the tax?

-

Will owners be able to dispute their assigned property values?

-

Will expensive pied-à-terre owners flood the rental market with their units in lieu of paying the additional tax?

Stay tuned for the answers as this is implemented and takes shape.

If you have or want a pied-à-terre and this is wigging you out, call me for the full scoop (that’s an ice cream joke).